Business Income Taxes in Illinois: How Are They Calculated?

Business Income Taxes in Illinois: How Are They Calculated?

June 2023 (76.4)

This article provides a high-level overview of how Illinois’ income tax applies to businesses. Most people have a basic understanding of the individual income tax, and there are many similarities, but it is important to understand this revenue source, particularly when evaluating the consequences (and advisability) of proposed changes.

Step-By-Step

All taxpayers follow the same basic process when determining how much income tax they owe in Illinois. It can get complicated, but the underlying fundamentals are the same for everyone, from a minimum wage-earner to a multimillion-dollar corporation:

1. Calculate the tax base

2. Determine Illinois’ share

3. Multiply by the tax rate

4. Apply any available credits

We will address each of these steps in turn, although there is one preliminary question to answer: is the taxpayer subject to Illinois income tax at all? In the tax world, this is called “nexus.”

Nexus. Income tax nexus standards vary from state to state, and there are also federal statutory and constitutional nexus limitations. Generally speaking, a business has nexus in Illinois (and therefore must file an Illinois income tax return) if it has employees or assets in the state.

Step One: Calculating the Tax Base

Illinois and most states rely on the federal government to do much of the heavy lifting for this step. Illinois is considered a “rolling conformity” state; changes to the Internal Revenue Code’s tax base provisions are automatically incorporated into Illinois’ tax base.

A quick note about individual taxpayers: For individuals, the starting point for Illinois taxes is federal adjusted gross income, which means that most of the federal deductions (like the standard deduction and itemized deductions like the one for home mortgage interest) are not taken into consideration. Illinois has its own personal exemption and there are a few other adjustments, perhaps most notably the deduction for federally taxed social security and other retirement income.

For businesses, the starting point in calculating Illinois income tax liability is federal taxable income. This is generally the business’s operating profits, after deductions for business expenses have been taken. Illinois requires a number of adjustments, decoupling from certain federal provisions and sometimes replacing them with our own alternative (in the case of depreciation, for example) and sometimes making adjustments to compensate for odd mismatches or to avoid unconstitutional results (in the case of the foreign dividends received deduction, for example).

Step Two: Apportionment (if necessary)

If a business operates solely in Illinois, Illinois income tax is paid on 100% of its taxable income. Things get more complicated, however, for businesses operating in multiple states. Multistate businesses are, naturally, subject to income tax in multiple states. It wouldn’t be fair (or constitutional) for each of those states to tax 100% of every business’s income, so states use what is called “formulary apportionment” to determine how much of a business’ income is taxable by that state. As its name suggests, formulary apportionment attributes a portion of a business’s income to Illinois using a mathematical formula. Since 2001, most businesses in Illinois have apportioned income according to the percentage of their gross receipts earned in Illinois—commonly called the single sales factor apportionment method. Apportionment methods vary by state, but a single sales factor apportionment method is the most common.

Illinois originally used a three factor apportionment formula, giving equal weight to:

1. The percentage of a business’s total property located in a state.

2. The percentage of a business’s total payroll paid to employees in a state.

3. The percentage of a business’s total sales made to customers in a state.

Over the years, states moved away from the three-factor formula and towards formulas that more heavily weighted the sales factor. This had the effect of reducing the tax burden on businesses with significant operations in the taxing state and “exporting” the burden onto businesses based elsewhere. The single sales factor apportionment method is often considered an economic development tool: businesses increasing their in-state presence through new investment and employees will see no increase in their apportionment, and therefore will not see an increase in their income tax liability merely because they invested in the state.

Step Three: The Tax Rate

This is a seemingly straightforward step. Calculating the tax base and determining how much of it Illinois can tax is generally the hard part, while multiplying that result by the tax rate is simple math. Illinois is a flat rate state, with no tax brackets or graduated rate structures to worry about, making it even simpler. However, different types of business entities can be subject to different tax rates, so a discussion of those entity types and their tax treatment is necessary.

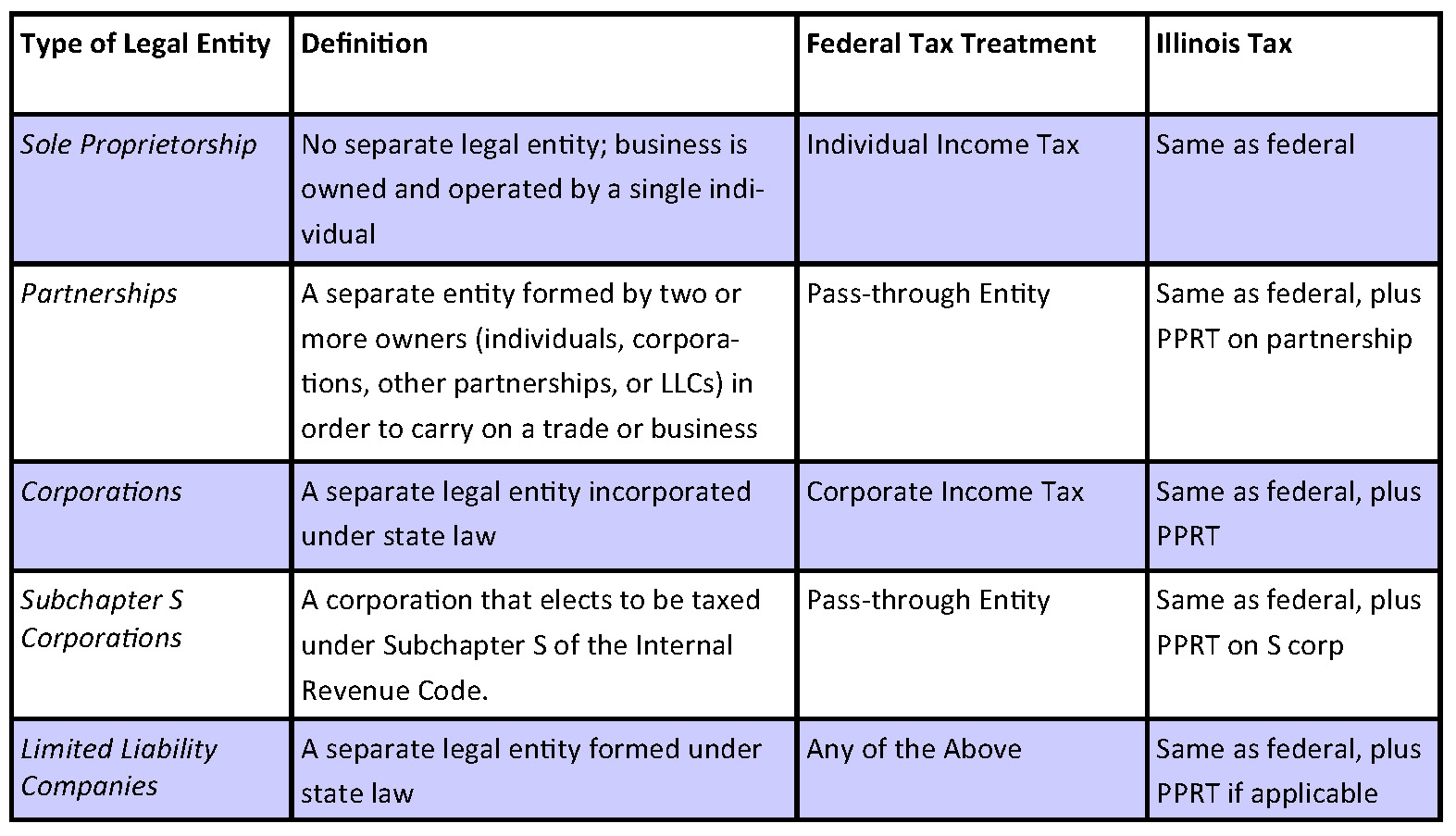

What tax, and tax rate, is paid on a business’s profits – whether it is corporate income tax (7.0%), individual income tax (4.95%), or the personal property tax replacement income tax (a unique-to-Illinois surtax often called the “Replacement Tax,” or “PPRT”) (1.5% or 2.5%), or some combination of the three – depends on the business’s organizational structure and on elections made with the IRS. Generally speaking, Illinois taxes business forms in the same way as the federal government, as discussed and summarized in the table below.

Corporation. The corporate form is often considered the “traditional” legal entity used by businesses. The corporate income tax rate in Illinois is 7%, and corporations also pay PPRT at 2.5%, for a total income tax rate of 9.5%.

Frequently, medium and large businesses operate through several different legal entities. This can be for a number of reasons, from regulatory requirements to a legacy of growth through mergers and acquisitions. States differ in their approaches to taxing these related entities. Illinois uses “combined reporting”, which requires a business to combine the profits and losses (and other tax attributes) of its related entities onto a single tax return. Other states use “separate accounting”, where each legal entity is taxed independently.

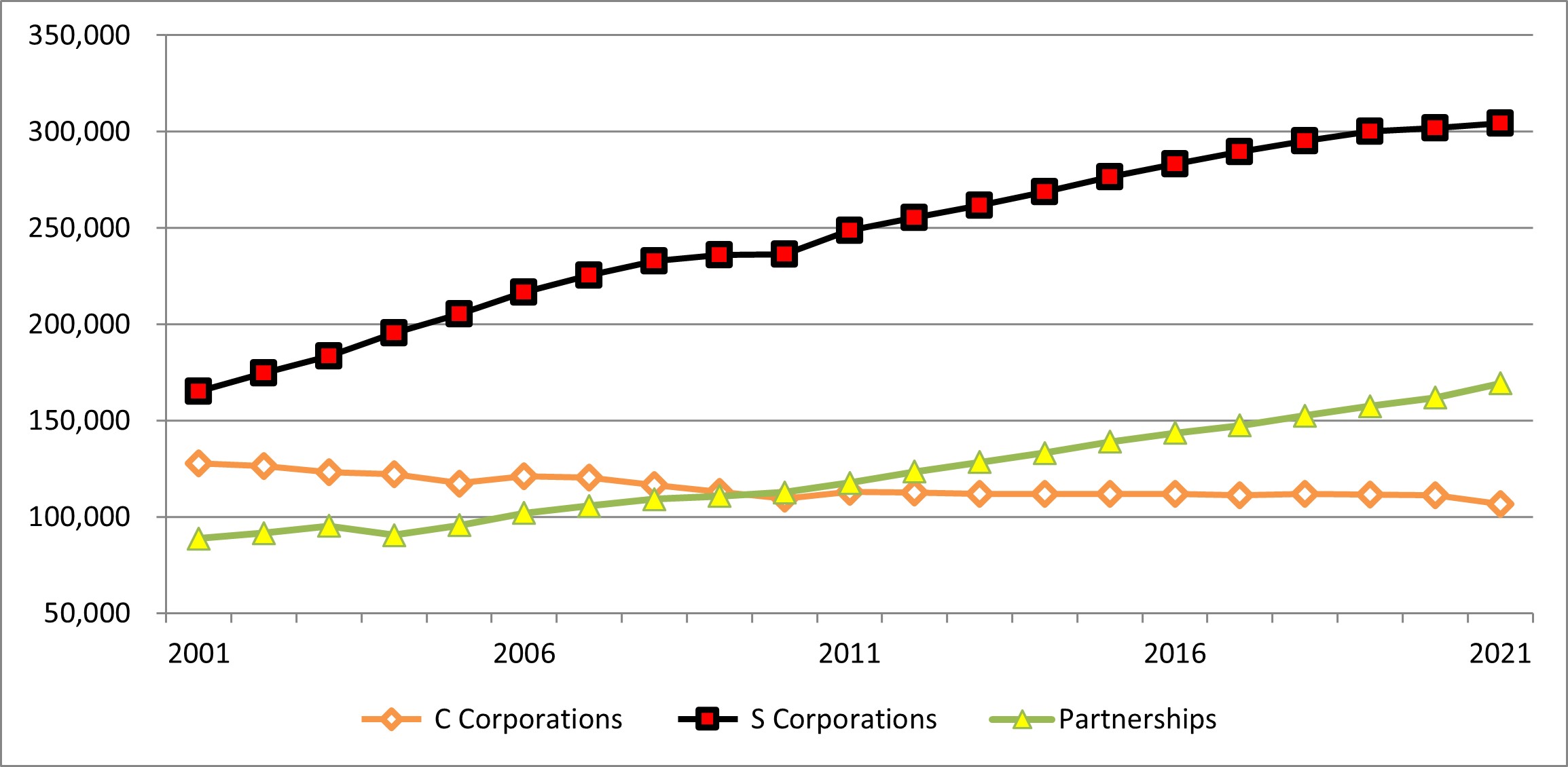

As indicated in the chart below, the corporate form of doing business has become less and less popular over the years, in part because of concerns over double-taxing of corporate income. As discussed above, a corporation’s profits are taxed at the entity level. Then, if the profitable corporation pays dividends to its owners, they are frequently also taxed on that dividend income—effectively taxing the same profits twice.

If a corporation meets certain requirements it can elect to be taxed under Subchapter S of the Internal Revenue Code. An “S corporation” becomes a pass-through entity, which we address next.

Pass-through Entities. S corporations and partnerships are commonly referred to as “pass-through entities” or “flow-through entities” because for tax purposes, their profits are passed through to their owners (whether any cash payments are made or not). These entities file annual informational returns but do not pay federal income tax. Instead, each owner (a partner in the case of a partnership, or an S corporation’s shareholder) pays tax on its share of the entity’s taxable income. Illinois follows the federal treatment of pass-through entities, taxing the owners rather than the entities, with one significant (and unique-to-Illinois) difference: the entity also owes PPRT.

The PPRT rate for pass-through entities is 1.5%. The owners are taxed on their distributive share of partnership or S corporation income at their own income tax rate, which, as this section makes obvious, varies with the type of owner.

Note: there is a new election available to pass-through entities to effectively pay the owners’ Illinois income tax at the entity level, in addition to the PPRT. The owners (partners or S corporation shareholders) will get an offsetting credit against their tax on the pass-through income. The credit was enacted (in Illinois and many other states) so that individuals could still get the full federal tax benefit of a tax deduction for state taxes paid, even though there is now a limitation on the itemized deduction for that expense; if the tax is paid at the entity level, the owner’s share of income that is passed through reflects the deduction at the entity level and the itemized deduction rules do not come into play for that entity-level expense. Whether the election is made or not, the tax rate on this income is the same.

Sole Proprietorship. A sole proprietorship is not a separate legal entity; it is a business owned and run by one individual with no legal distinction between the owner and the business. The business’s income or loss is calculated and reported by the owner on his or her individual income tax return, combining it with any other income or losses the owner might have (if, for example, a ride-share driver has a full or part-time job as well). This is true at the federal and Illinois level.

Illinois’ tax rate for individuals is 4.95%, so that’s the rate applicable to taxable business income earned by a sole proprietorship.

Limited Liability Company. A limited liability company, or LLC, is a legal entity that can be taxed like sole proprietorships, partnerships, corporations or S corporations, depending on the number and nature of owners and the elections filed with the IRS. Illinois follows the federal characterization of LLCs, and the preceding discussions apply to LLCs falling into those classifications.

Step Four: Credits

The final step in calculating a business’s Illinois tax liability is to apply any credits against the tax calculated in Step 3. There are a number of credits that may be available to individual and business taxpayers. They are more commonly used by individuals (for things like the Earned Income Tax Credit, or Illinois’ credit for property tax paid), but there are a variety of economic development-related credits for businesses.

For a more thorough explanation of Illinois’ largest tax expenditures and the policy rationales behind them (or lack thereof), see the April 2021 issue of Tax Facts.

Business Entity Returns Filed in Illinois

Conclusion

All Illinois taxpayers follow the same basic process when computing their tax liability, once it is clear they have nexus and must file and pay Illinois income tax: calculate the tax base, determine what portion of it is taxable by Illinois, multiply by the tax rate, and apply any available credits. In a future issue of Tax Facts, TFI will estimate how much of Illinois’ total income tax revenue is attributable to business profits and how much is attributable to income earned through wages or investments by individuals—as this discussion makes clear, it is not a straight-forward calculation, and has become more complicated over the years.